Down payment assistance programs help Washington homebuyers overcome the biggest barrier to homeownership: the upfront cash requirement. These programs offer grants and loans that can significantly reduce or even eliminate your down payment.

Quick Answer: Washington State Down Payment Assistance Options

- Statewide programs: Up to $40,000 through WSHFC programs.

- King County: Up to $45,000 for eligible areas, depending on the program.

- Tacoma: Up to $80,000 for qualified homebuyers.

- Snohomish County: Up to $50,000 in assistance.

- Specialized programs: Additional funds for veterans and those affected by historical discrimination.

The dream of Washington homeownership is within reach, even without a 10% or 20% down payment. Many potential buyers can afford the monthly payments but struggle with the large lump sum needed to buy.

Here’s the reality: You might qualify for assistance even if a lender has told you otherwise. Many programs don’t require you to be a first-time buyer, and some have no income limits at all.

Washington boasts a comprehensive network of DPA programs, from statewide options to generous local aid in cities like Tacoma. We also offer some private programs that don’t have the limitations of the programs offered by cities, counties, and the state. The key is understanding your options and navigating the application process effectively.

How Does Down Payment Assistance Work in Washington?

Down payment assistance programs bridge the financial gap between your savings and the upfront costs of buying a home. They reduce your initial burden, allowing you to purchase a home sooner in Washington’s competitive market, where prices can climb faster than you can save.

What are the different types of DPA?

Washington offers several types of assistance, each with different advantages:

- Grants: This is gift money that doesn’t need to be repaid, provided that you meet certain conditions (like staying in the home for a set period).

- Deferred payment loans: The most common type in Washington state. Repayment is postponed until you sell, refinance, or pay off your first mortgage. Many, like the Home Advantage DPA, are zero-interest loans deferred for up to 30 years or until you sell your house.

- Forgivable loans: These loans are forgiven over time. If you stay in your home for a specific period (e.g., 5 to 15 years), the debt disappears.

- Low-interest loans: These function as second mortgages with regular payments but at a much lower interest rate than market rates.

Most DPAs come in the form of a second mortgage with desirable terms, often with no monthly payments until you sell or refinance.

How does DPA work with your main mortgage?

Down payment assistance programs pair seamlessly with almost every type of home loan, including FHA, VA, and conventional loans. Even if you qualify for a zero-down VA loan, DPA can help cover the closing costs.

To use these programs, you must work with a participating lender approved by the DPA provider. Your lender will coordinate your primary mortgage and the assistance loan, ensuring that all the paperwork works together smoothly. In some cases, you can even combine assistance from multiple programs to significantly increase your buying power.

Ready to explore how you might buy with minimal upfront costs? Check out our comprehensive guide on buying a home with no money down to see all your options.

Exploring Statewide and Local Down Payment Assistance

Washington has a wealth of down payment assistance programs from the state, cities, and counties. The primary statewide provider is the Washington State Housing Finance Commission (WSHFC), but local programs often provide larger amounts of aid.

Washington State Housing Finance Commission programs

Washington State Housing Finance Commission programs

The WSHFC offers several popular DPA programs that pair with their affordable first mortgages:

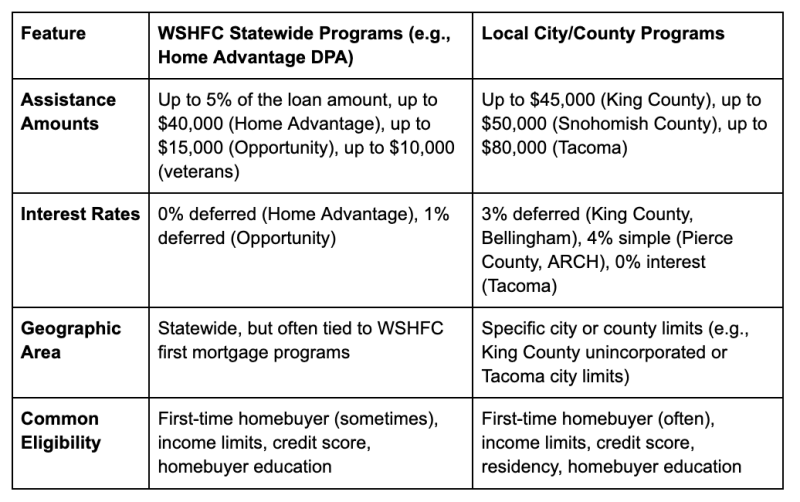

- Home Advantage Program: Provides up to 5% of the loan amount as a 0% interest, deferred loan. In our opinion, this is the premier option offered by the WSHFC. Learn more about the Washington State Home Advantage Program.

- Opportunity DPA Program: Offers up to $15,000 as a 1% deferred loan for low- to moderate-income buyers.

- Veterans DPA Loan: Provides up to $10,000 in assistance for veterans and active-duty service members.

- HomeChoice Program: Offers up to $15,000 for eligible buyers with a disability or who have a household member with a disability.

To access these programs, you must work with a WSHFC-approved lender. As specialists in these loans, we can guide you through the entire process and ensure that all requirements are met.

City- and county-specific programs

Many local jurisdictions offer generous DPA programs with specific geographic restrictions:

- King County DPA: Up to $45,000 as a 3% deferred loan in unincorporated areas and certain cities.

- Snohomish County DPA: Up to $50,000 in assistance.

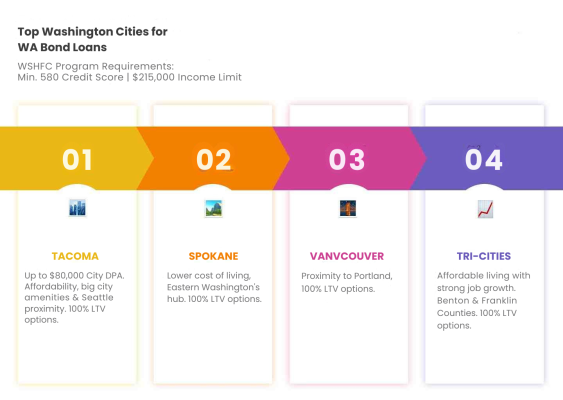

- Tacoma DPA: Up to $80,000 as a 0% deferred loan.

- Bellingham DPA: Up to $40,000 as a 3% simple interest deferred loan.

- Other local programs: Pierce County (up to $24,900), ARCH East King County (up to $30,000), and the city of Pasco also offer assistance.

Program availability can fluctuate, as seen with a recently reserved Clark County program, which quickly ran out of funds.

Who Can Benefit from Washington’s DPA Programs

While Washington’s down payment assistance programs are designed to help a broad range of homebuyers, certain groups face unique challenges that make these programs particularly valuable. Understanding how DPA can specifically benefit different professions and communities helps you see where you might fit in this landscape of opportunity.

Essential workers: Teachers, nurses, and first responders

Washington recognizes that many of the people who keep our communities running—teachers, nurses, firefighters, and police officers—often struggle to afford homes in the areas they serve. This creates a troubling cycle where the people who educate our children and keep us safe can’t afford to live in the communities where they work.

Teachers are a critical part of our communities, and many of these programs work well for them. In addition, we offer some programs with reduced lender fees for teachers.

Healthcare workers and first responders frequently qualify for multiple assistance options due to their moderate incomes and community service. Many nurses, EMTs, and firefighters find themselves in the sweet spot for income-based programs—earning too much for the lowest-income assistance but not enough to easily save for down payments in Washington’s expensive housing market.

These essential workers often benefit most from programs with flexible income limits and the ability to combine multiple assistance sources.

Rural families: Accessing homeownership outside urban centers

Rural Washington families face a unique set of challenges and opportunities when it comes to homeownership. While property prices are generally lower in rural areas, access to financing and assistance programs can be more limited.

USDA Rural Development Loans pair exceptionally well with down payment assistance for families in eligible rural areas throughout Washington. Communities in counties like Ferry, Adams, Grant, parts of Skagit, and several other counties often qualify for 100% USDA financing, meaning that families can purchase homes with no down payment requirement.

When you combine USDA loans with available DPA programs, rural families can often cover closing costs and still have funds available for moving expenses or immediate home improvements. This is particularly valuable for families purchasing older rural properties that may need updates.

Agricultural workers and small-business owners in rural areas often have irregular income patterns that can make traditional lending challenging. DPA programs that focus on overall financial stability rather than strict month-to-month income requirements can be game-changers for these families.

Young professionals and first-time buyers

Washington’s tech industry and growing economy attract many young professionals who can afford monthly mortgage payments but struggle to save large down payments while paying rent in expensive urban areas.

Tech workers and young professionals in Seattle, Bellevue, and other tech hubs often find themselves caught between high salaries that disqualify them from some programs and living costs that make saving difficult. However, several programs have income limits high enough to include moderate-income tech workers, especially those just starting their careers.

The Home Advantage Program, for instance, doesn’t have the strict income caps of some local programs, making it accessible to young professionals who earn decent salaries but haven’t had time to build substantial savings. We also have $0 down payment programs with no income limits at all.

Recent graduates carrying student debt particularly benefit from programs that don’t require perfect debt-to-income ratios. Some buyers find that using DPA allows them to maintain emergency funds while still achieving homeownership, providing financial security during the early years of homeownership.

Families affected by historical discrimination

Washington has created specific pathways for families whose homeownership opportunities were historically limited by discriminatory practices.

The Covenant Homeownership Program specifically serves families with ancestors who faced housing discrimination in Washington before 1968. This includes many Black, Asian American, Latino, and Native American families whose ancestors were prevented from building generational wealth through homeownership.

Single parents and nontraditional households

Single-parent households often face the dual challenge of supporting a family on one income while trying to save for homeownership. Washington’s DPA programs recognize these challenges in several ways.

Many programs have flexible definitions of “first-time homebuyer” that specifically include displaced homemakers and single parents who may have previously co-owned a home. This acknowledges that life changes—divorce, death of a spouse, or other circumstances—can put homeownership temporarily out of reach.

Income calculations for single parents often work favorably with DPA programs, as the assistance can make the difference between qualifying for a mortgage and falling short of debt-to-income requirements.

Military families and veterans

Veterans and active-duty service members have access to some of the most generous combinations of assistance available. The Veterans DPA Program provides up to $10,000, which can be combined with the benefits of VA loans (no down payment, no private mortgage insurance).

This combination is particularly powerful because veterans can use DPA funds for closing costs while the VA loan covers the purchase price. For military families who move frequently, this flexibility is invaluable.

Military families stationed at Joint Base Lewis-McChord find themselves in a unique position, with access to VA loans and down payment assistance options, they can often buy a home easier than they thought possible.

Making the most of available programs

The key insight for all these groups is that Washington’s down payment assistance landscape is designed to serve working families—people who contribute to their communities but may need help overcoming the initial financial hurdle of homeownership.

Whether you’re a teacher in Spokane, a nurse in Vancouver, a tech worker in East King County, or a veteran in Tacoma, there’s likely a combination of programs that can help make homeownership achievable. The most successful buyers are those who work with lenders experienced in navigating these various programs and can identify the best combination of assistance for their specific situation.

Remember that some of these programs can be combined, and eligibility requirements vary significantly. What matters most is understanding that these programs exist because Washington recognizes that homeownership should be accessible to the people who make our communities strong.

The Path to Approval: Eligibility and Application Steps

Understanding the qualification and application steps for Washington’s down payment assistance programs is your next move. While each program has unique rules, many share similar criteria.

Who qualifies for down payment assistance in Washington?

DPA programs are more accessible than you might think. Here are the common requirements:

- Income limits: Most programs are for low- to moderate-income households, based on your county’s area median income (AMI). However, some of our exclusive programs have no income limits at all!

- Credit score requirements: A minimum credit score of 580 is a common benchmark. If your score is lower, we can offer guidance on how to improve it. See our credit tips for buying a home with no down payment in Washington.

- Homeownership history: Many programs are for “first-time homebuyers,” defined as anyone who hasn’t owned a home in the past three years. This often includes displaced homemakers or single parents. Better yet, some of our exclusive programs don’t require you to be a first-time homebuyer.

- Property eligibility: The home must be your primary residence and fall within the program’s purchase price and geographic limits.

Your application roadmap: From class to keys

Navigating the DPA application is manageable with the right guidance.

1. Find a participating lender: This is crucial. You need a lender who is approved for and experienced with DPA programs. We specialize in matching buyers with the right programs and ensuring a smooth, coordinated process.

2. Submit your application: Your lender will help you prepare and submit both your primary mortgage and DPA applications, which include income verification, credit reports, and other documents. Working with an experienced team makes all the difference.

3. Homebuyer education: Most DPA programs require homebuyer education. However, different programs require different courses. Ask your lender which homebuyer education you should take.

4. One-on-one counseling: Some programs require personalized housing counseling to review your budget and ensure that you’re ready for homeownership. We will let you know if that is required for the program you use.

A Special Opportunity: The Covenant Homeownership Program

Washington state’s groundbreaking Covenant Homeownership Program goes beyond typical down payment assistance. It’s a form of restorative justice designed to address the lasting harm caused by historical housing discrimination.

What is the Covenant Homeownership Program?

For decades, legal documents called racial covenants barred people of color from buying homes in many Washington neighborhoods, creating a wealth gap that persists today. The homeownership rate for Black households in greater Seattle (26%) is roughly half that of white households (51%).

Passed in 2023 with bipartisan support and championed by groups like the Black Home Initiative, this act acknowledges that historical discrimination created lasting financial barriers. The program provides assistance to families directly impacted by these past injustices.

Eligibility and how to apply

This program has very specific requirements tied to Washington’s pre–civil rights era.

- Who qualifies: You must be a first-time homebuyer whose household income is at or below 100% of the area median income (AMI). In addition, you or a direct ancestor (parent, grandparent, or great-grandparent) must have lived in Washington before April 1968 (when the Fair Housing Act passed) and belonged to a racial or ethnic group that faced housing discrimination.

- Documentation: You’ll need to provide documents proving your ancestor’s pre-1968 residency and racial/ethnic background. This can include birth certificates, school or church records, Census data, or genealogical records.

- How to apply: The first step is to work with a commission-trained lender who can help you pre-qualify for a mortgage and verify your eligibility for the program. For guidance, you can also call the Washington State Homeownership Hotline at 1-877-894-4663.

For complete details, speak with a trained loan officer.

Weighing the Pros and Cons of Down Payment Assistance

Like any financial tool, Washington’s down payment assistance programs have both incredible benefits and important considerations.

The benefits of using DPA

The advantages of DPA can be life-changing for Washington homebuyers:

- Lower upfront costs: Keep your emergency fund intact instead of draining your savings for a down payment.

- Faster homeownership: Get into the market sooner, which is a huge advantage as home prices rise. Waiting to save can be costly, as our article on the cost of waiting to buy explains.

- Build equity sooner: Your monthly payment builds your own wealth, not a landlord’s.

- Reduced financial stress: Buying a home without emptying your bank account provides peace of mind.

- Increased buying power: Assistance can help you afford a home that better fits your long-term needs.

What are the drawbacks of down payment assistance programs?

It’s also important to be realistic about the potential challenges:

- Repayment obligations: Most down payment assistance is a loan, not a grant. It typically must be repaid when you sell the home, refinance, or move out.

- Selling or refinancing triggers: Your flexibility may be limited, as a sale or refinance will trigger the loan repayment.

- Potential for higher interest rates: Some DPA programs may come with a slightly higher interest rate on your primary mortgage.

- Program limitations: You may face restrictions on property location, purchase price, or home type. Funding can also be limited and may run out.

For most buyers, the benefits far outweigh these considerations. A knowledgeable lender can help you choose a program that aligns with your long-term goals.

Frequently Asked Questions About DPA in Washington

We get these questions daily from hopeful homebuyers. Down payment assistance programs can seem complex, but understanding the basics shows how many doors they can open.

How much money can I actually get?

The amount varies dramatically by location and program. Statewide programs through the WSHFC typically offer up to $40,000. However, local programs are often more generous:

- Snohomish County: Up to $50,000

- King County: Up to $45,000

- Bellingham: Up to $40,000

- Tacoma: Up to $80,000

It’s sometimes possible to combine programs for even greater assistance. We specialize in helping you identify and stack all the aid you qualify for to maximize your benefits.

Do I have to be a first-time homebuyer?

This is a common misconception. While many state and local programs require you to be a “first-time” buyer (defined as not owning a home in the past three years), this definition is broad. Displaced homemakers and single parents who previously co-owned a home often qualify.

More importantly, some of our exclusive programs have no first-time buyer requirement at all, opening up opportunities for repeat buyers.

What if I don’t qualify for these programs?

Don’t worry, there are always alternatives. If traditional DPA isn’t a fit, we can explore other paths to homeownership with little money down:

- Lender-specific programs: We have access to programs that don’t rely on government aid, some with no income limits and flexible requirements.

- Gift funds: Most loan types allow relatives to gift money for your down payment.

- Seller concessions: In some market conditions, sellers may agree to pay a portion of your closing costs.

- Government-backed loans: USDA loans offer 100% financing in eligible rural areas, while FHA loans require only 3.5% down with flexible credit guidelines.

The bottom line is that homeownership shouldn’t be out of reach. We find creative solutions for buyers in all situations. See more ideas in our video Buying a Home with No Money Down.

Your Next Step Toward Washington Homeownership

These programs break down the intimidating down payment barrier, making homeownership possible. The landscape of assistance is broader than most people realize—you don’t always need to be a first-time buyer, and some programs we offer have no income limits.

The key to success is having expert guidance. The world of DPA can be overwhelming, but our team at WA Bond Loans thrives on this complexity.

We have built our reputation on understanding the ins and outs of Washington’s assistance programs, including exclusive options that many borrowers don’t know exist. We believe everyone deserves a chance at homeownership and take the time to match you with the programs that best fit your goals.

Ready to find out exactly how much assistance you might qualify for? Let’s create a personalized roadmap to make your homeownership dreams a reality.

Explore your down payment assistance options today.