WA Bond home loans are down payment assistance programs that help Washington residents buy their first home with little to no money down. These programs provide a second mortgage to cover your down payment, often with deferred repayment terms that make homeownership accessible even if you don’t have thousands saved.

Quick facts about WA Bond home loans:

- What they are: Down payment assistance loans (second mortgages).

- Assistance amount: Up to 5% of home price (potentially $40,000+ on higher priced homes).

- Repayment: Most are deferred until you sell, refinance, or pay off your primary mortgage.

- Credit requirement: Most programs do not have a minimum credit score, but the first mortgage typically requires at least a 580 credit score.

- Income limits: Vary by program, county, and household size. Some programs have no income limit.

- Compatible with: FHA, VA, USDA, and conventional loans.

For some families, the dream of homeownership in Washington state crashes into a major roadblock: the down payment. With high median home prices, saving 10% to 20% for a down payment can delay your plans to buy a home.

But here’s what most people don’t know: Washington offers some of the most generous down payment assistance programs in the country through the Washington State Housing Finance Commission (WSHFC). These programs can provide thousands of dollars to help cover your down payment and closing costs.

The key is understanding how these programs work and finding a lender who has access to them. Many traditional banks don’t participate in these specialized programs, which is why so many potential homebuyers get turned away, thinking they need to save for years before they can buy.

What Are WA Bond Home Loans, and How Do They Help You Buy a Home?

WA Bond home loans are your ticket to homeownership when saving for a down payment feels impossible. These down payment assistance (DPA) programs work like a financial bridge. They provide the money you need upfront to buy your home, typically through a second mortgage that you don’t have to worry about paying back right away.

Here’s the beautiful part: While you’re focused on making your regular mortgage payment each month, that assistance loan just sits there quietly in the background. No monthly payments, no immediate stress. It’s what we call “deferred payments,” and it’s a game-changer for families who want to buy now instead of waiting years to save up.

The Washington State Housing Finance Commission (WSHFC) oversees most of these programs, and it has created some fantastic options. Their Home Advantage Program has helped thousands of Washington families get into homes.

Don’t confuse these home purchase programs with rental bond assistance. That’s completely different and helps with security deposits for rentals. We’re talking about buying your home with down payment assistance, not renting.

Understanding the loan structure

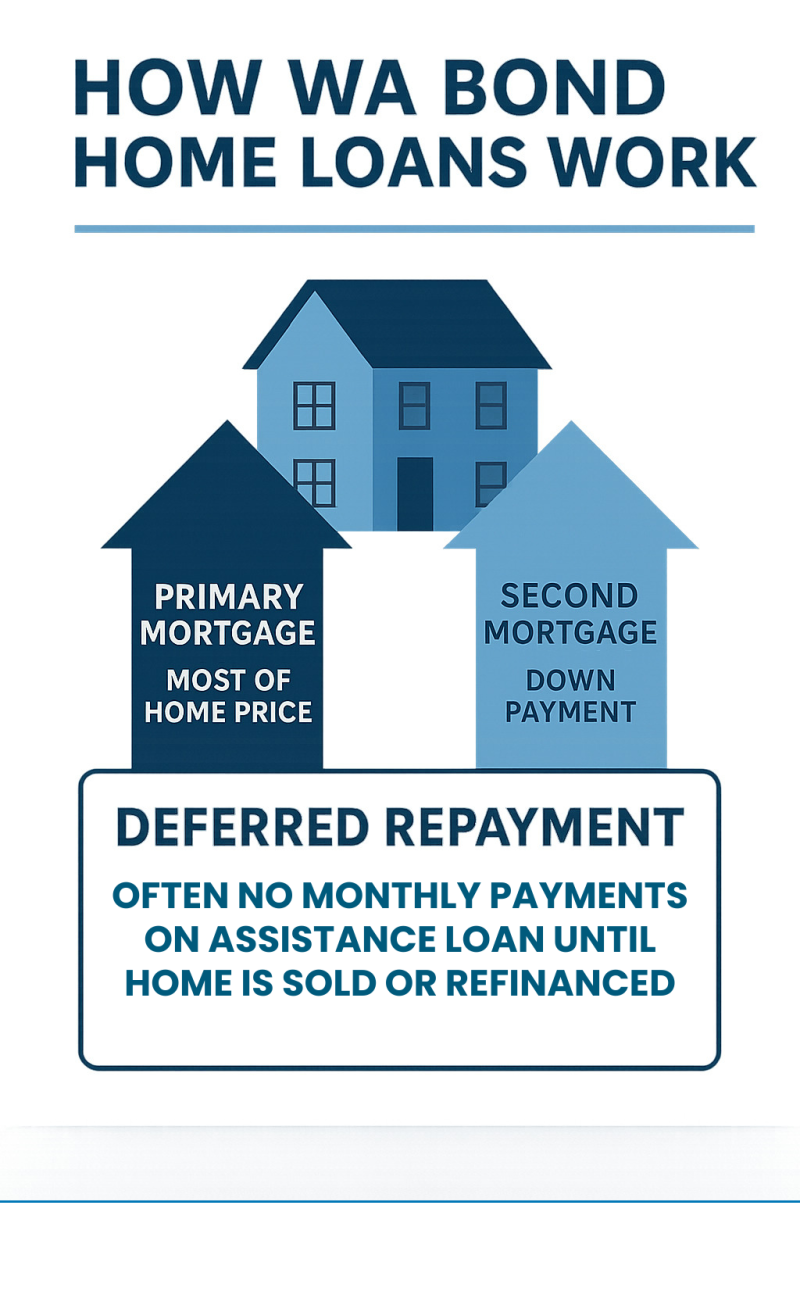

Think of your WA Bond home loans assistance as a helpful second mortgage, or what lenders call a “second lien.” You’ll have your main mortgage doing the heavy lifting, as well as this smaller loan covering your down payment and sometimes closing costs, too.

The magic happens with the repayment terms. Most of these assistance loans are either forgivable (meaning they disappear over time if you meet certain conditions) or deferred (meaning you pay them back later when specific things happen). With deferred loans, you typically repay when you sell your home, refinance your primary mortgage, or pay off that main loan completely.

Interest rates on these assistance loans are usually very favorable. But here’s where it gets exciting: You can potentially get up to 5% of your home’s purchase price in assistance. On a $400,000 home, that’s $20,000. On an $800,000 home? That’s a whopping $40,000 helping you get those keys in your hand.

How Do I Know if I’m Eligible for a WA Bond Home Loan?

“Will I actually qualify for this?” The good news is that WA Bond home loans and other down payment assistance programs are designed to help regular Washington families, not just a select few.

There are many different programs, and it can be confusing. That is why your first step should be to speak with a knowledgeable loan officer who can help you determine the best loan they have to offer.

Let’s start with the basics. Most programs require a minimum credit score of 580. If you’re thinking, “Uh-oh, my credit isn’t perfect,” don’t panic! A 580 score isn’t asking for perfection; it’s showing lenders you’re responsible with money.

Beyond credit scores, you’ll encounter income and asset requirements that vary among programs. Most programs also require you to complete a homebuyer education course. Don’t worry, it’s not like going back to school! These courses are pretty helpful and teach you things like how to maintain your home and manage your mortgage payments.

There are a few different education requirements, so make sure you ask your lender which course applies to the program you are going to use.

Income limits

Many traditional WA Bond home loan programs set household income limits, but these limits can shift based on your household size and where you’re buying in Washington. After all, living costs in Seattle versus Spokane are pretty different.

The great news here is that one of the best programs has a household income limit of $215,000. And another private program has no income limit at all.

Pairing Your Assistance with the Right First Mortgage

Here’s something important to understand: WA Bond home loans don’t work alone. They’re designed to team up with a primary mortgage to make your home purchase happen. Your main mortgage does the heavy lifting by covering most of the home’s price, while the down payment assistance steps in to handle what you can’t cover upfront. That said, both the primary mortgage and the down payment assistance second mortgage are offered as a package.

The tricky part? You need a lender who knows how to make these programs work together. It’s frustrating, but many traditional banks either don’t participate in these specialized programs or simply don’t understand how to coordinate them properly. That’s where working with the right lender makes all the difference.

We specialize in seamlessly combining these loans because we believe homeownership shouldn’t be out of reach just because you haven’t saved tens of thousands of dollars. You can start your Washington home search with no down payment today.

Comparing mortgages compatible with DPA

The good news is that WA Bond home loans work with several different types of first mortgages. Each one has its own personality and benefits, so let’s break down your options:

- FHA loans are incredibly popular for first-time buyers because they’re forgiving with credit scores and require only 3.5% down. When you combine that small down payment requirement with down payment assistance, you’re looking at very little money needed upfront.

- VA loans are an amazing benefit for our veterans and active military members. Since they already offer 0% down, pairing them with assistance means you can use those funds for closing costs instead. It’s a powerful combination that can get you into a home with virtually nothing out of pocket.

- USDA loans serve rural communities with 0% down requirements. If you’re looking at homes in eligible rural areas, this could be your golden ticket to homeownership.

- Conventional loans typically require stronger credit, but they offer great flexibility once you qualify. They work beautifully with down payment assistance and often have fewer restrictions than government-backed loans.

How much down payment assistance can I get?

The amount of assistance available through WA Bond home loan programs isn’t just a flat dollar amount. It often scales with your home’s price.

Many programs offer assistance up to 5% of your home’s purchase price. Let’s put that in real numbers: If you’re buying an $800,000 home (which isn’t uncommon in Washington), 5% assistance equals $40,000. That’s life-changing money that can make the difference between renting for years and owning your home today.

Here’s another bonus: These funds aren’t limited to just your down payment. In most cases, you can also use the assistance to cover closing costs. This flexibility means you could potentially walk into your closing with very little cash needed from your own pocket—sometimes even none at all when everything aligns perfectly.

Your Step-by-Step Guide to Applying for Assistance

Getting your WA Bond home loan assistance doesn’t have to feel overwhelming. Hundreds of Washington families have gone through this process, and honestly it’s much simpler than most people think. The key is having the right guide, and that’s where we come in.

Step 1: The housing options assessment

Before we can find you the perfect WA Bond home loan program, we need to understand your financial picture. This isn’t about judging your spending habits or making you feel bad about your savings account balance. It’s about finding your strengths and matching you with the best assistance available.

We’ll start with an assessment of your finances. This means looking at your income, your current debts, and your credit score. If you’re not sure what your credit score is, no problem—we’ll help you check that, too. The goal is to get a clear, honest picture of where you stand so we can show you exactly what’s possible.

You’ll need to gather some documents for this step, but nothing too crazy. We’re typically talking about recent pay stubs, bank statements, and your W-2’s from the past couple of years. Having these ready can speed things up quite a bit.

This initial assessment often reveals that you’re in better shape than you thought. Many of our clients are pleasantly surprised to learn they qualify for programs they didn’t even know existed.

Step 2: Finding a participating lender and getting pre-approved

Here’s where working with us makes all the difference. While you could try to steer this process with a traditional bank, you’d likely hit a wall pretty quickly. Many lenders simply don’t participate in these specialized WA Bond home loans, and virtually none have access to the exclusive programs we offer.

Getting pre-approved is your golden ticket in Washington’s competitive housing market. When sellers see that pre-approval letter, they know you’re serious and that you can actually close on the deal. We’ll pre-approve you for both your primary mortgage and your down payment assistance, so you’ll know exactly how much house you can afford.

The pre-approval process also helps us determine which specific DPA programs you qualify for. Maybe you’re eligible for the standard WSHFC programs, or maybe you’re a perfect fit for one of our exclusive offerings. Either way, we’ll make sure you get the maximum assistance available.

Wondering how much you can afford with these programs? You can get started with us today.

Frequently Asked Questions About WA Bond Home Loans

We get a lot of questions about WA Bond home loans—and, honestly, that’s exactly what we want! Understanding these programs is crucial to making the best decision for your homeownership journey. Let’s explore the most common questions we hear every day.

Are WA Bond home loans interest-free, and do they need to be repaid?

WA Bond home loans for home purchases are loans, not free money. But this is still amazing news for you.

These down payment assistance loans are structured very differently from your typical loan. While they do need to be repaid eventually, most come with deferred payment terms. This means you won’t be making monthly payments on your DPA loan alongside your regular mortgage payment.

Instead, the loan becomes due when specific life events happen. You’ll need to repay it when you sell your home, when you refinance your primary mortgage, or when you pay off your main mortgage completely. Think of it as a patient loan that waits until you’re in a better position to handle it.

You might be thinking about those rental bond assistance programs you’ve heard about from the Department of Communities. Those are typically interest-free, but they’re for renters, not homebuyers. The WA Bond home loans we specialize in may accrue interest over time, but since the payments are deferred in many cases, your monthly budget stays manageable.

This deferred structure is what makes homeownership possible for so many Washington families. You get the help you need now, and you deal with repayment later when you’re likely in a stronger financial position.

What is the difference between government-offered bond rental assistance and home purchase bond loans in WA?

The term “bond assistance” gets thrown around a lot in Washington, and it can mean completely different things depending on your situation.

Government rental bond assistance is what you might find through the Department of Communities. These programs help people pay security deposits and advance rent for rental properties. They’re interest-free and have strict limits—like keeping your assets under $5,000 if you’re single or $10,000 for couples. Over 10,000 of these loans get approved each year, but they’re all about helping people rent homes, not buy them.

WA Bond home loans are entirely different. These are down payment assistance programs that help you buy a home. While these programs are government-backed, you typically access them through specialized private lenders like us.

What types of home loans are compatible with the WA Bond home loans program?

One of the best things about WA Bond home loans is how flexible they are. These programs can work with most major types of home loans, which means we can find a combination that fits your specific situation perfectly.

- FHA loans are probably the most popular pairing with DPA programs. They’re federally insured, which means lenders can offer them with lower down payments and more flexible credit requirements. If your credit isn’t perfect, this combo might be your golden ticket to homeownership.

- VA loans are incredible for our military families. If you’re an eligible veteran, active-duty service member, or surviving spouse, you can get a VA loan with zero down payment and then use WA Bond down payment assistance funds to help with closing costs. It’s like getting a double benefit for your service.

- USDA loans work great if you’re looking at homes in eligible rural areas. These also offer zero down payment. When combined with DPA, you might find yourself buying a home with almost no money out of pocket.

- Conventional loans are the traditional option that works well when you have good credit and a stable income. They offer competitive rates and flexible terms, especially when paired with down payment assistance.

While most WA Bond home loans play nicely with these loan types, some specific programs have their own preferences. Certain DPA programs might work better with FHA loans, while others are more flexible. That’s where our expertise really shines. We know which combinations work best and can guide you to the perfect match for your situation.

Want to explore your options? Start your home search in Washington with no down payment today.

Resources:

Home Advantage Program