The best Washington cities to buy a home with WA Bond home loans include Tacoma, Spokane, Vancouver, and the Tri-Cities region. These areas combine affordable housing with robust down payment assistance (DPA) programs, creating ideal conditions for homebuyers.

While Washington’s median home price of $630,700 can feel overwhelming, Washington State Housing Finance Commission (WSHFC) programs can provide up to $40,000 in down payment assistance, with some cities offering even more local support.

All that said, the best city for you is the city you want to live in. Remember, while the cities below have some advantages, many programs are available statewide.

Top Washington cities for WA bond home loans:

- Tacoma: Up to $80,000 in down payment assistance

- Spokane: Lower cost of living with 100% loan-to-value options

- Vancouver: No state income tax (unlike Oregon) with 100% LTV options

- Tri-Cities: Strong job growth and affordable home prices, with 100% LTV options

These bond loan programs use tax-exempt bonds to offer competitive interest rates and substantial down payment help. You don’t need perfect credit; many programs accept scores as low as 580. The best locations combine reasonable home prices with strong local economies and additional city-specific assistance.

What Are WA Bond Loans, and How Do They Work?

WA Bond home loans are state-sponsored mortgage programs designed to make homeownership more affordable. The Washington State Housing Finance Commission creates these programs using mortgage revenue bonds. The state issues tax-exempt bonds, which allow it to offer lower interest rates and significant down payment help.

The two main programs are the Home Advantage program and the House Key Opportunity program. Both are designed to help you buy a home without a big upfront investment.

The process involves getting a competitive 30-year fixed-rate mortgage through an approved lender, which can be an FHA, VA, USDA, or conventional loan. Alongside your primary mortgage, you receive down payment assistance (DPA) in the form of a second mortgage.

This down payment assistance makes WA bond loans accessible. Instead of needing tens of thousands of dollars upfront, you might need only a few thousand, or sometimes nothing at all. Many of these down payment assistance loans have deferred payments, meaning you don’t make monthly payments on them until you sell, refinance, or pay off your primary mortgage.

What are the benefits of using the WA Bond home loan program?

The benefits of using the WA Bond loan program extend beyond down payment assistance:

- Lower upfront costs are the biggest benefit for most buyers. The Home Advantage program allows down payment assistance of almost 5% of the purchase price. That can be up to $40,000 in some cases. This allows you to focus on finding the right home instead of saving for years.

- Closing cost assistance is another key benefit. Many DPA programs can also cover some of your closing costs, which can range from $5,000 to $15,000, making your path to homeownership smoother and more affordable.

- Competitive fixed interest rates are also a benefit thanks to the bond financing structure. This means lower monthly payments and significant savings over the life of your loan.

Statewide availability means these programs can be used throughout Washington, whether you’re looking in Spokane, Tacoma, or anywhere else in Washington state.

Most importantly, you can combine WA Bond loans with FHA, VA, USDA, and conventional loans. This flexibility allows you to stack benefits, such as using a zero-down VA loan with additional down payment assistance from WSHFC.

What are the eligibility requirements of the WA Bond home loan program?

While we offer some exclusive programs with even more flexibility, standard WSHFC programs have straightforward requirements:

- Your credit score needs to be at least 580 for most programs, including the Washington State Home Advantage Program. If your score needs work, we can help you take steps to improve it as you prepare to buy your home.

- You must complete a homebuyer education course, which covers everything from budgeting to home maintenance, to prepare you for confident homeownership. We will help you find the right course to take.

- Finally, your debt-to-income ratio should generally be 50% or lower, ensuring that you can comfortably manage your mortgage payments. However, we can support modestly higher debt-to-income ratios in some cases.

What Are the Best Cities to Buy a Home Using the WA Bond Loan Program?

When considering the best Washington cities to buy a home with WA Bond loans, we look for locations where your dollar stretches furthest. The ideal cities combine affordability, thriving job markets, and local down payment assistance programs that can be stacked with state benefits.

With Washington’s median home price at $630,700 as of September 2025, homeownership can seem out of reach. However, we have found that certain cities offer incredible opportunities where your WA Bond loan can work twice as hard. These locations are where we’ve seen families successfully become homeowners, often with minimal cash out of pocket. They offer reasonable home prices, strong local economies, and generous local programs that add tens of thousands in additional help.

All that said, the best city for you is the city you want to live in. Remember, while the cities below have some advantages, many programs are available statewide.

Tacoma: Affordability meets big-city amenities

Located in Pierce County, Tacoma offers big-city amenities without the high price tag. You get urban living, from cultural attractions to diverse dining, but your housing dollar stretches further than in nearby Seattle. The proximity to Seattle is a major benefit for commuters, and Tacoma also has its own thriving economy centered around the Port of Tacoma.

For bond loan users, the City of Tacoma Down Payment Assistance program is a standout. It offers up to $80,000 in assistance for down payment and closing costs. When combined with WSHFC bond loan benefits, this creates a powerful package that makes homeownership surprisingly affordable.

Spokane: Eastern Washington’s hub for first-time buyers

Spokane has a reputation as one of the most buyer-friendly markets in the state. The cost of living is more reasonable than in Western Washington, meaning that you may be able to afford a home more easily here than in some western parts of the state such as Seattle or Bellevue.

The city’s job market is diverse, with strong opportunities in healthcare, technology, and education. This provides stable employment for homeowners. The Spokane area has experienced steady growth with less rapid price hikes than seen in some other markets.

Spokane Neighborhood Action Partners (SNAP) offers assistance programs that can help buyers achieve 100% loan-to-value financing, potentially allowing you to finance the entire purchase price.

Vancouver: A smart choice in Clark County

Vancouver offers the benefits of both Washington and Oregon. You can work in Portland’s robust job market while enjoying Southwestern Washington’s more relaxed lifestyle. The city sits along the Columbia River, offering outdoor recreation and a growing downtown scene.

Also, if other household members work in Washington, you will not have to pay state income tax on their income thanks to Washington’s lack of state income tax, which can improve your budget and mortgage qualification.

The Tri-Cities (Kennewick, Pasco, Richland): Affordable living with strong growth

The Tri-Cities region is one of Washington’s best-kept secrets for homebuyers. Located in Benton and Franklin counties, this area offers affordable housing in a growing economy.

The economic foundation is solid, built on Hanford Site employment, agriculture, and a growing wine industry. The region has seen steady job growth without the housing price volatility of other areas, making it an excellent choice for building equity.

How Do I Apply for the WA Bond Loan Program?

The application process for a WA Bond home loan is manageable when broken down into steps:

- First, get pre-approved with an approved lender. This step involves reviewing your finances to determine how much home you can afford. A pre-approval shows sellers that you are a serious buyer and helps you focus your home search on properties within your budget.

- Next, complete a homebuyer education seminar. This required five-hour course covers budgeting, credit management, and the mortgage process, giving you the confidence and knowledge needed for homeownership. Your lender will help you determine the best homebuyer education course for your needs.

- Finally, gather your documents. Your lender will need recent pay stubs, your last two years’ W-2s, and recent bank statements. They may also ask for statements from retirement accounts or other assets. Having these documents organized will speed up the approval process.

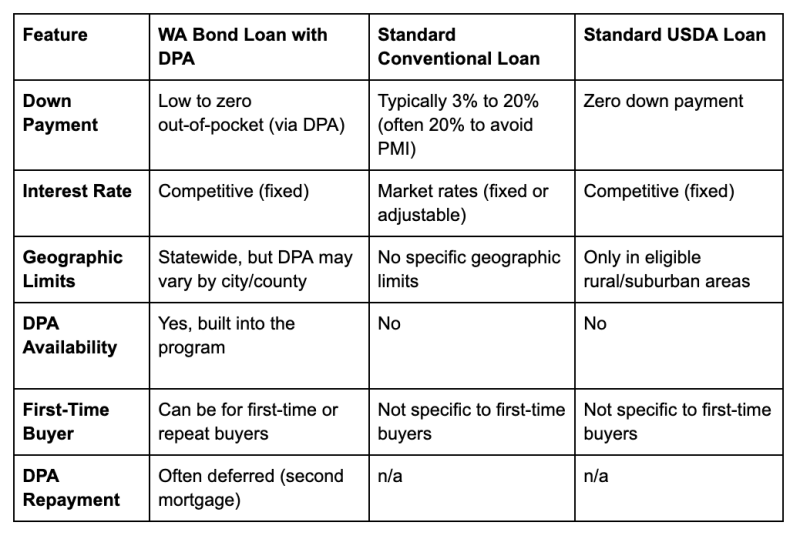

Comparing WA Bond Loans with Other Options

WA Bond loans offer unique advantages, particularly with down payment assistance, but it’s helpful to see how they compare with other options. While a conventional loan might require a down payment of $60,000 or more on a typical Washington home, and a USDA loan limits you to rural areas, WA Bond loans with DPA offer minimal out-of-pocket costs with the flexibility to buy in urban areas like Tacoma or Spokane.

Here’s how the main options compare:

The flexibility of WA Bond home loans is a key benefit. You can combine them with FHA, VA, conventional, or USDA loans to layer advantages and create a financing package that fits your needs.

WA Bond loans vs. USDA loans

Both USDA loans and WA Bond loans are excellent for minimizing upfront costs, but they serve different needs. USDA loans, backed by the U.S. Department of Agriculture, are for rural and suburban homebuyers. They require no down payment and accept credit scores as low as 640, but you are limited to USDA-eligible areas, which excludes most major cities.

USDA loans also typically require lower debt-to-income ratios. When you combine this with lower income limits, it can sometimes be hard to qualify for the home you want with a USDA loan.

Another main difference is location. If you want to live in an urban center, a USDA loan won’t work. Luckily, urban centers are some of the best Washington cities to buy a home with WA Bond loans.

You can sometimes combine programs: Use a USDA loan for a first mortgage in an eligible area and add WSHFC down payment assistance to cover closing costs.

Potential drawbacks of WA Bond loans

While WA Bond home loans are beneficial, it’s important to understand their structure.

- The down payment assistance is a second mortgage. While payments are often deferred for years, it is a loan that must be repaid eventually, typically when you sell or refinance.

- Repayment terms vary. Some DPA loans are interest-free, while others charge a low rate, like 1% or 3% with deferred payments. It’s crucial to understand the terms of your specific loan.

- The sale or refinance clause means the DPA loan usually comes due when you sell your home or refinance your first mortgage.

- Your first mortgage interest rate might be slightly higher than that of a conventional loan without DPA. However, the thousands saved on a down payment usually make this a worthwhile trade-off.

- Program requirements like income limits, credit score minimums, and homebuyer education courses mean the programs are not for everyone. Still, they are designed to be achievable for most middle-income buyers.

If you’re wondering if you qualify for down payment assistance with a WA bond loan, contact us today. We’ll help you navigate the process of buying your home in Washington.

Frequently Asked Questions About WA Bond Loans

Here are answers to some of the most common questions we receive about WA Bond loans.

Can I use a WA Bond loan if I’m not a first-time homebuyer?

Yes, you can use a WA Bond loan even if you’ve owned a home before. The Home Advantage program is open to both first-time and repeat homebuyers.

Additionally, the WSHFC uses a generous definition of “first-time homebuyer.” Under their three-year rule, you are considered a first-time buyer if you haven’t owned and occupied a primary residence in the past three years. This means that if you have sold a home, gone through a divorce, or experienced other life changes, you may still qualify for programs like House Key Opportunity, which are geared toward first-time buyers.

What property types are eligible for WA Bond loans?

WA Bond home loans offer flexibility in property types, allowing you to find a home that fits your lifestyle.

- Single-family homes, the traditional detached houses, are the most common option.

- Condominiums and townhomes are also eligible, provided the complex meets FHA, VA, or conventional loan approval standards.

- Manufactured homes can qualify if they are permanently attached to land you own and meet HUD and FHA guidelines.

- Multi-unit properties with up to two units can qualify. This allows you to buy a duplex, live in one side, and rent out the other, as long as you occupy one unit as your primary residence.

The main rule is that the property must be your primary residence. Investment properties and vacation homes do not qualify.

Ready to find out how much assistance you qualify for? Connect with us and let’s turn your homeownership dreams into reality.

Resources:

Washington State Housing Finance Commission

Washington State Home Advantage Program

NWMLS home price statistics

Spokane Neighborhood Action Partners (SNAP)

City of Tacoma Down Payment Assistance